#1 Savings Hack All Self-Employed People Need To Know

Working for yourself has some incredible benefits — freedom from early-morning alarms, rigid work schedules, boring daily routines and stifling...

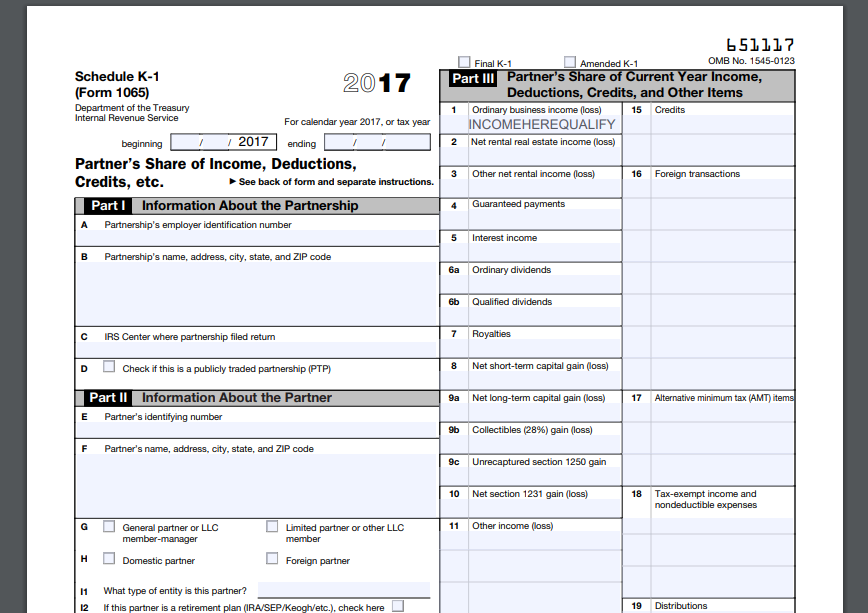

In order to be eligible for the Self-Directed Solo 401(k) account, you must be self-employed and have no full time employees. Further eligibility requirements and exceptions below.

You and your spouse are the only people who can own the business. There can be no other outside ownership, or you will not qualify for the Solo 401(k).

To qualify for a Self-Directed Solo 401(k), you cannot have any full-time common law employees other than your spouse. You can have part-time employees, but if you hire full-time employees in the future, you will have to stop contributing or come up with another retirement plan solution (maybe a SEP-IRA).

My other business has employees... but not the one I want to connect to the Solo 401(k). Does that still count?

Yes, unfortunately. The IRS can see this as hiding a retirement plan from your employees in another business. If you have employees, you can be subject to "discrimination testing" to make sure that if you are giving yourself retirement benefits or an employer match, that your other employees are also eligible for fair employer match and able to contribute to retirement accounts.

If you ignore this, you could be subject to retirement backpay or legal action from your employees as a violation of ERISA law by enforcement of the Department of Labor. (DOL)

.png)

Working for yourself has some incredible benefits — freedom from early-morning alarms, rigid work schedules, boring daily routines and stifling...

You know those annoying infomercials that clog up the late-night airwaves as they hawk everything from perfect abs to greaseless grills? Well, you...

Rocket Dollar provides customers unparalleled access to a wide range of alternative investments, from real estate to private equity to...