A Solo 401(k) is a retirement plan that can be used by the self-employed. If you're self-employed and looking to set up a retirement plan, then a Solo 401(k) might be right for you. In this article, we'll discuss what it's like to have a Solo 401(k), how much it costs to set up and maintain, and who qualifies for one in order to help you make an informed decision about whether or not this is the right option for your specific situation.

Who is eligible for a Solo 401(k)?

- You're self-employed. If you have a business that is not incorporated, you can open a Solo 401(k).

- You are a sole proprietor or partner in a partnership. If you are self-employed and work as an independent contractor, you may be eligible for a Solo 401(k).

- Your spouse is also self-employed. You can include your spouse’s earned income from their own business when calculating the maximum annual contribution to your Solo 401(k). Since spouses are allowed to make catch-up contributions up until April 15th of the following year (after turning 50), this allows them to contribute more money towards retirement!

What are the benefits of a Solo 401(k) to you?

- You can make tax-deductible contributions.

- You are not taxed on earnings until withdrawal.

- You can take out loans from your 401k.

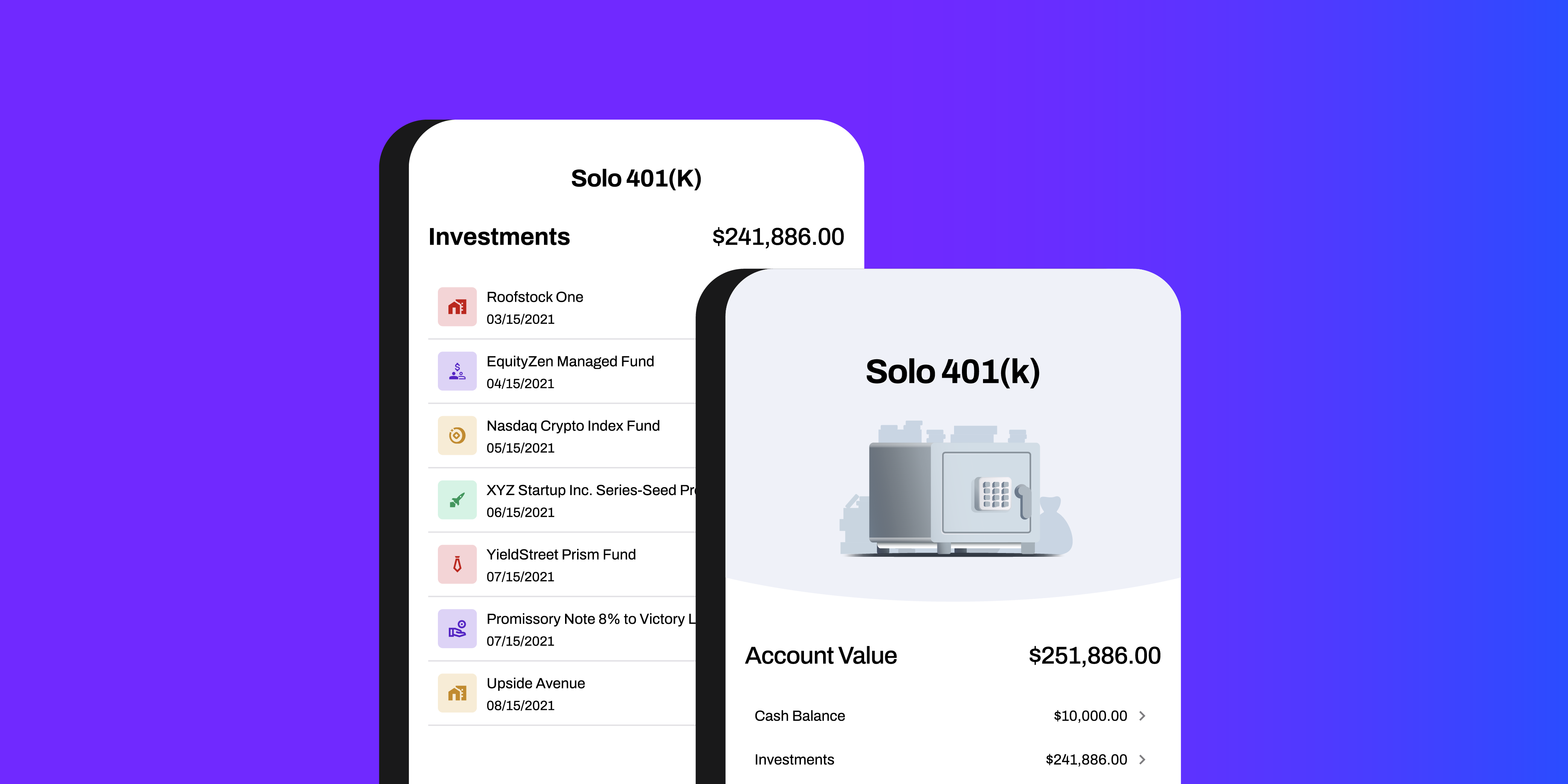

- You are free to invest in any asset class allowed by the IRS.

What are the rules for Solo 401(k) contributions?

The pre-tax/tax-deferred contribution types for a Solo 401(k) plan for each plan participant and the same amounts for their spouses include the salary deferral and the business contribution up to the total maximum annual Solo 401(k) contributions of $61,000 in 2022 (not including any catch-up contributions for those 50 or older). This limit is the same as a SEP IRA.

Contributing the same maximum amount for yourself and your spouse may potentially double the maximum limit for a married couple to $102,000.

For the salary deferral contribution, a plan participant may contribute 100% of earned income up to the maximum amount allowed, which is $20,500 in 2022.

The business contribution is up to 25% of your income, which is your net self-employment earnings after deducting 50% of your employment tax and contributions for yourself.

Catch-up contributions of an extra $6,500 per year in 2022 are possible for those aged 50 or older.

If allowed by a customized Solo 401(k) plan, optional contributions include after-tax contributions held in a Roth 401(k) subaccount.

Do I need an investment advisor for my Solo 401(k)?

Solo 401(k) plans can be managed by you, your spouse, or any other person who has access to the account. You don’t need to hire an investment advisor if you want to manage your own account. You can use a robo advisor, a financial planner, and/or work with an individual stockbroker that specializes in retirement accounts or other investments (like real estate). If you want help creating and managing your investment strategy for your Solo 401(k), this may be beneficial for you.

A Solo 401(k) could be an excellent retirement plan option if you are self-employed.

If you are self-employed, a Solo 401(k) could be an excellent retirement plan option. A Solo 401(k) is a great way to save for retirement and reduce your taxes.

A Solo 401(k) can be a great retirement plan for people who are self-employed. It's easy to set up and maintain, allows for contributions from both your employer and yourself, and it has many of the same benefits as other types of plans (like 401k plans). But it does require some additional work on your part, so you'll need to decide whether or not that's worth it in order to get started with this type of retirement account.

Thomas Young

Thomas Young

.png)