Henry Yoshida

Henry Yoshida

Is a Solo 401(k) Right For You?

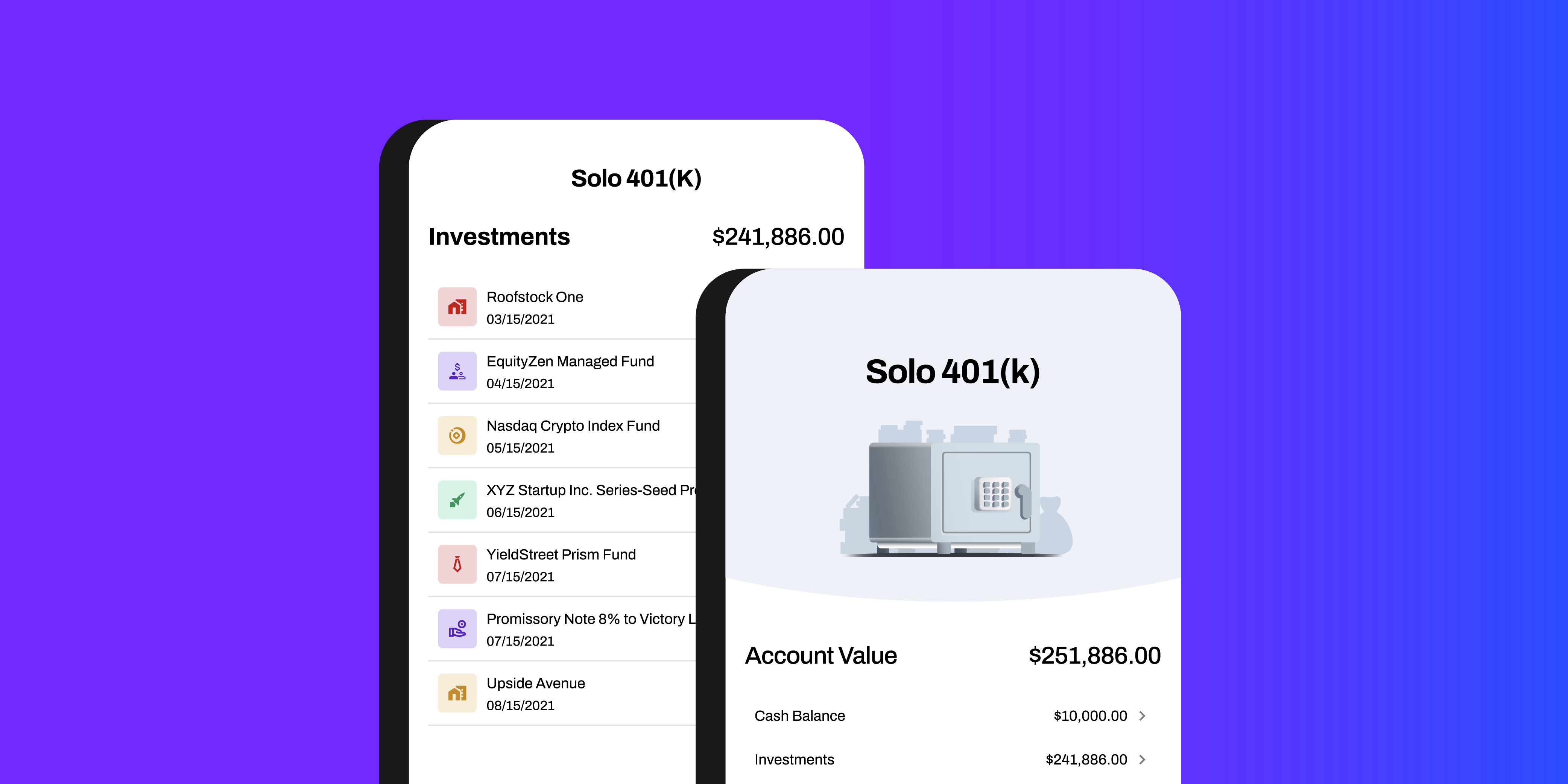

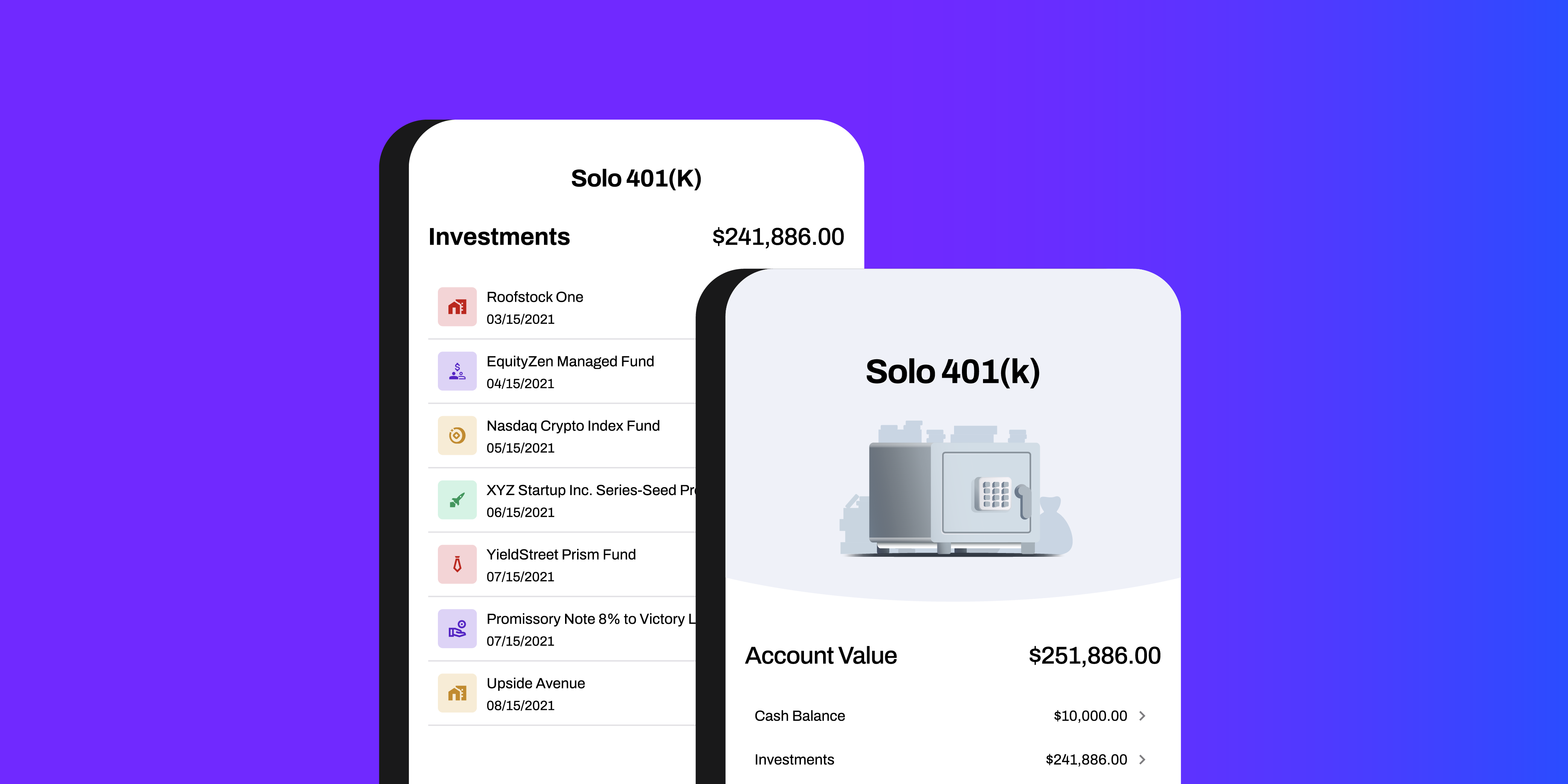

A Solo 401(k) is a retirement plan that can be used by the self-employed. If you're self-employed and looking to set up a retirement plan, then a...

Choosing between a Solo 401(k) plan (also known as a one-participant 401(k) plan) and a simplified employee pension (SEP) plan is kind of like choosing between a ribeye from Morton’s or one from Ruth’s Chris—both are excellent options. Let’s take a closer look at the benefits of both plans and the situations for which each is particularly well suited.

Both types of retirement plans are good options for saving, and it’s always best to have some type of savings plan in place to help provide enough money to last the duration of your retirement. For some retirement investors, putting their money into a Solo 401(k) can be more advantageous because these plans provide more flexibility.

Here are the three main benefits a Solo 401(k) offers over a SEP:

With a Solo 401(k), you can borrow up to 50% of the total balance with a $50,000 cap. If you pay the loan back on time, there are no taxes or penalties for borrowing from yourself. In essence, you become your own rich uncle. Loans typically must be paid back in five years, or 15 years if the loan is used to purchase a primary residence. The loan can be used for any purpose.

Opening a SEP typically requires using an individual retirement account (IRA) custodian. However, with a Solo 401(k), you act as the plan’s custodian. Since you are the plan’s administrator and its trustee, you can manage investments from your IRA without needing to work through a third-party administrator. You also can save on fees since there aren’t any administrative or management fees with a Solo 401(k).

There’s no Roth IRA conversion option for SEPs, and Roth IRAs provide some key tax advantages. All Roth contributions are made with post-tax dollars, so portfolio growth is 100% tax-free.

SEP plans are primarily used to help employees of small businesses create their retirement nest eggs. Business owners can make contributions up to 25% of each employee’s pay—employees aren’t eligible to make contributions to their SEP-IRAs. Contributions are tax-deductible for employers, and growth accrues tax-free until the employee retires and begins taking distributions.

Here are three main reasons why a SEP-IRA may make sense for certain individuals and small business owners over a Solo 401(k):

Unlike most qualified employer-sponsored IRAs, which have high setup and custodial management fees, SEP-IRAs are easy to establish and have low administrative costs. Plus, plan expenses may also be tax-deductible.

While Solo 401(k)s are primarily used by individuals and independent contractors with no employees, SEP-IRAs can be established by a wide range of business owners, including partnerships, corporations and sole proprietors.

Since employers are responsible for all contributions to the SEP-IRA, they can forgo contributions in times of economic distress or low annual profits.

Contribution limits with both SEP-IRAs and Solo 401(k) plans for 2021 are $58,000. However, Solo 401(k) plans allow for a “catch-up” contribution of up to $6,500 if you are over age 50 (the IRS calls these “elective deferrals”), which boosts the annual contribution limit to $64,500. Since employers make all contributions to SEP-IRAs, there’s no option for employees to make elective deferrals.

Both plans can be advantageous in certain situations. Solo 401(k) plans can be easier to self-manage because they require less paperwork than SEP-IRAs, which require filing an IRS form 5498 annually regardless of the account’s value. A SEP-IRAs may be ideal for small businesses whose employees are financially limited and therefore might not be able to make significant contributions to their retirement accounts, while a Solo 401(k) may be the better option for people who can afford to make the lion’s share of contributions to their retirement savings. Ultimately, the choice of either type of retirement savings plan should be weighed carefully and discussed with a financial professional.

A Solo 401(k) is a retirement plan that can be used by the self-employed. If you're self-employed and looking to set up a retirement plan, then a...

For entrepreneurs, freelancers, and self-employed individuals, it can sometimes feel like your retirement account options are limited. Traditional...

When choosing an alts-capable retirement account, choosing the right type of account can have a significant impact on your flexibility and ease of...