Josh Plave

Josh Plave

NASDAQ Congratulates Rocket Dollar In Times Square

Rocket Dollar reached a new milestone in Q3 of 2019: customers in all 50 states and $50M assets under management, and NASDAQ recognized the milestone...

Did you know that in certain situations, your Self-Directed IRA can incur taxes? While you might be wondering how a retirement account can generate taxable income, it’s important to understand the underlying concepts and the impact they may have in order to make the right investing decisions.

![]()

Josh Plave is a multifamily investor that helps people grow their retirement accounts by using methods that can free them from reliance on the stock market. Josh founded Wall to Main to illustrate the power in your existing IRA or 401k and show you how to take greater control of your future.

To begin, we need to learn what Unrelated Debt-Financed Income is and when it can rear its ugly head. For a better understanding, let’s break up the phrase. Starting with Unrelated, in this situation it means “not yours” aka—not from your retirement account. In other words, you’re bringing in funds from elsewhere. Debt-Financed is pretty obvious; it just means deriving from debt, or a loan. And finally we have Income, the money received from the unrelated debt or loan. So in whole, UDFI means any income derived from using debt brought in from outside your retirement account.

When Congress created the IRA in 1974, the intent was to incentivize you to use tax-deferred dollars to save for your future self. By using borrowed money from a bank or lender, your tax-deferred dollars are benefitting from the use of non–tax-deferred dollars. The IRS is okay with this, they just require you to pay tax on this type of behavior.

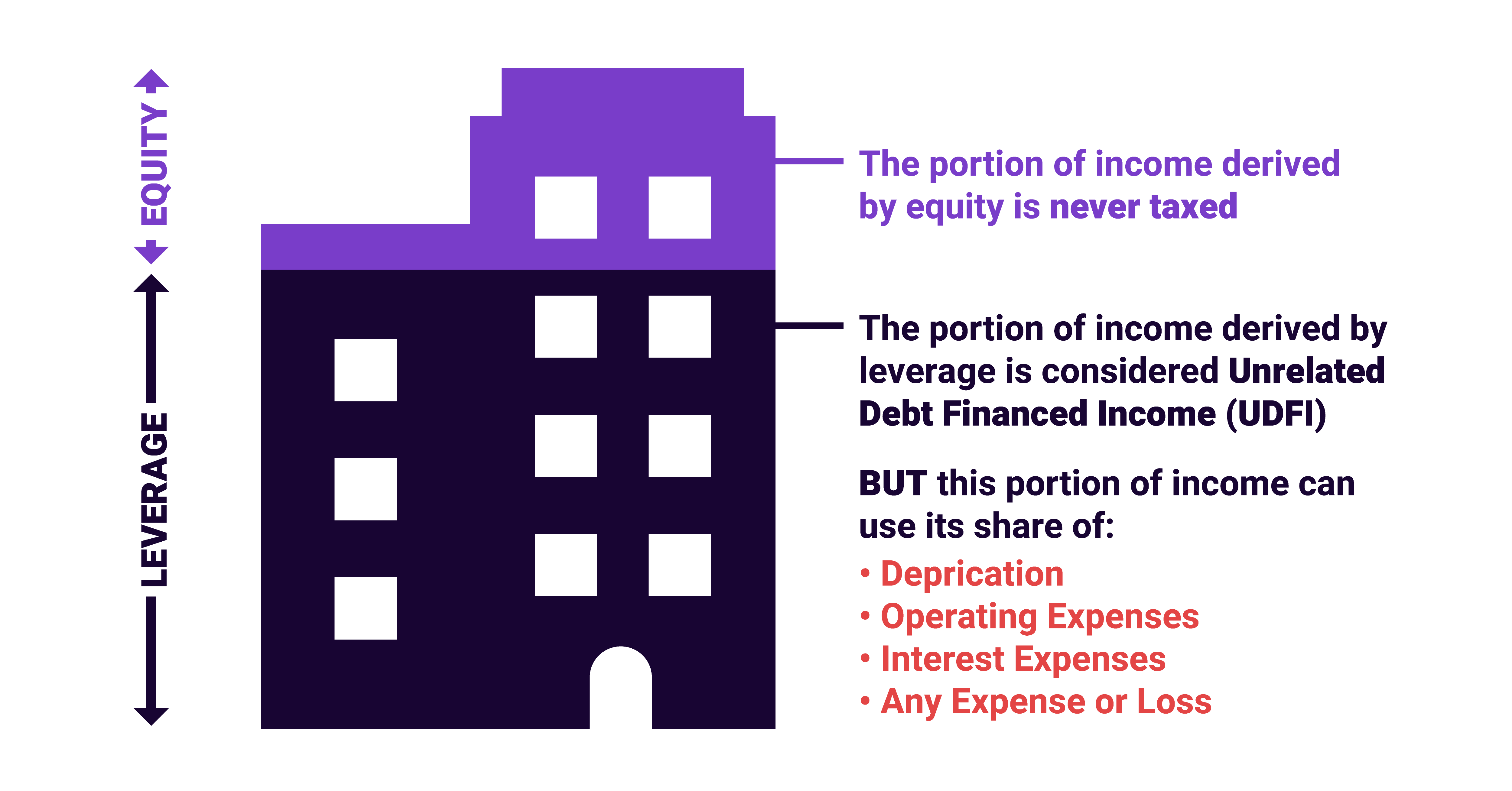

Luckily, the high paper losses generated by real estate can help offset your tax burden. Let’s take a look at this hypothetical investment we’ll be making with our Self-Directed IRA.

We made a 25% down payment, illustrated up top in light purple to signify the equity we have in the project. The remaining 75% of the deal is leveraged, utilizing debt from a lender.

So, income earned by the equity in our Self-Directed IRA is never taxed. However, with this investment, 75% of the income was earned by leverage and would be considered UDFI. Now, the nice thing about this is because it’s income derived from someone else’s money, this portion of income can actually make use of its leveraged share of losses.

So we can take advantage of depreciation, operating and interest expenses, or really any other expense or loss generated by the property. In the first year, we can use approximately 75% of those losses and expenses, and as the debt is paid back, this ratio between equity and debt begins to change.

The tax that UDFI generates is called Unrelated Business Income Tax, also known as UBIT.

UBIT is calculated using the trust tax rate table, which just like any other tax has both an income and a capital gains rate table. Additionally, UBIT is paid directly from your Self-Directed IRA, never from your personal funds.

Wall to Main has built the first ever UBIT Calculator. For any multifamily investment opportunity, they can calculate the annual taxes they’d expect to see through the life of a project. This allows for their investors to gain a clearer understanding of how much they’ll be left with after paying taxes on cash flow and sales proceeds.

Provided to their investors on every opportunity they offer, their UBIT Calculator is highly robust, adjusting for refinances, interest-only periods, and even varying investment amounts.

When investing in a multifamily property, they’ve typically found that:

If you plan to use your Self-Directed IRA to invest in a leveraged asset, these concepts apply to you.

Just remember: Your IRA earns UDFI, and pays UBIT. UDFI is income, UBIT is tax.

Get your FREE copy sent straight to your inbox now!

Rocket Dollar reached a new milestone in Q3 of 2019: customers in all 50 states and $50M assets under management, and NASDAQ recognized the milestone...

Understanding that pursuing early-stage investments is a must, we discussed how and why you can pair OurCrowd investments with a Rocket Dollar...

Over the last four years, we've built a powerful and flexible platform that allows investors to take advantage of alternative assets with their...